Historical Credit Score Files

Publication of additional historical credit score data

On July 1, 2026, Fannie Mae published historical credit score data for FICO® Score 10T and additional data for VantageScore® 4.0. This effort aims to enhance transparency and provide additional insights to our industry partners.

To support the industry in transitioning to the new credit score models, Fannie Mae is providing anonymous historical credit data.

Datasets are currently available representing loans acquired by Fannie Mae from approximately April 2013 to September 2025 (which closely aligns with applications/originations from approximately January 2013 to June 2025).

A key component of the newer credit score models is their use of trended data which is only available across all three credit bureaus starting from January 2013.

Access the Data

To access the historical credit score files, click on the Register/Login to download link provided below. New users must first register and accept the Terms and Conditions and Privacy Notice before downloading the files. Data Dynamics® users may use their existing credentials to log in to access the files.

Historical Credit Score Files

Register/login to download historical credit score files for Mortgage-Backed Securities (MBS) Disclosures, Historical Loan Performance, and Credit Risk Transfer (CRT) Datasets.

Download Historical Credit Score Files

Note: Due to the file size (10M+ records), files are meant to be consumed by advanced analytics programs.

Disclaimers: When using the historical credit score files, it is important for users to understand the following information on the data contained in the files.

- Historical credit score files contain FICO Score 10T and VantageScore 4.0 scores generated by Equifax, Experian, and TransUnion, each using the applicable bureau’s archived credit data. We do not make any representations or warranties concerning the quality, accuracy, or completeness of the historical data from these third parties or the adequacy or suitability of the historical credit files for any use or purpose.

- The type, content, format, structure, and quality of this data depends on how this data was collected and stored at the specific time the archive was created. This may be a different time than the time at which the credit report used at origination was generated for the loans included in the files. This difference in timing may lead to differences in credit scores between the archive credit data and the origination credit data.

- Archive credit data may not reflect more recent updates in the content and structure of credit reports. For instance, changes over time to the reporting of medical collections, tax liens, judgments, student loan forbearance, and rental payments (among other things) will not be reflected (if applicable) in scores generated based on credit data archived before those changes went into effect.

- The historical credit score files must not be used to, directly or indirectly, identify any specific individual. Users must comply with the Terms and Conditions, which contain important information on the permitted uses and restrictions for the data contained in the historical credit score files.

How to Use the Historical Credit Score Files with the Disclosure Datasets (MBS, Historical Loan Performance, and CRT)

When using the historical credit score files, it's important for users to understand that the “common” Loan Identifier matches the Loan Identifiers published in our disclosure datasets. The Loan Identifier does not correspond to the Fannie Mae Loan Number or Lender Loan Number. The historical credit score files are primarily intended to be combined with the MBS disclosures, or Historical Loan Performance or CRT datasets to perform analytics in accordance with any usage limitation in the Terms and Conditions.

What Loan Identifiers Will Match

| Historical Credit Score Loan Identifier | GSE Loan Number | Lender Loan Number | MBS Disclosures Loan Identifier | Historical Loan Performance Dataset Loan Identifier | CRT Dataset Loan Identifier |

|---|---|---|---|---|---|

| 5968784709 | |||||

| 100023020488 | |||||

| 136626329 |

Historical Credit Score Loan Identifier 5968784709 GSE Loan Number

Lender Loan Number

MBS Disclosures Loan Identifier

Historical Loan Performance Dataset Loan Identifier

CRT Dataset Loan Identifier

|

Historical Credit Score Loan Identifier 100023020488 GSE Loan Number

Lender Loan Number

MBS Disclosures Loan Identifier

Historical Loan Performance Dataset Loan Identifier

CRT Dataset Loan Identifier

|

Historical Credit Score Loan Identifier 136626329 GSE Loan Number

Lender Loan Number

MBS Disclosures Loan Identifier

Historical Loan Performance Dataset Loan Identifier

CRT Dataset Loan Identifier

|

Note: One additional attribute (besides the Loan Identifier) will be required to match the loan information across both data sets.

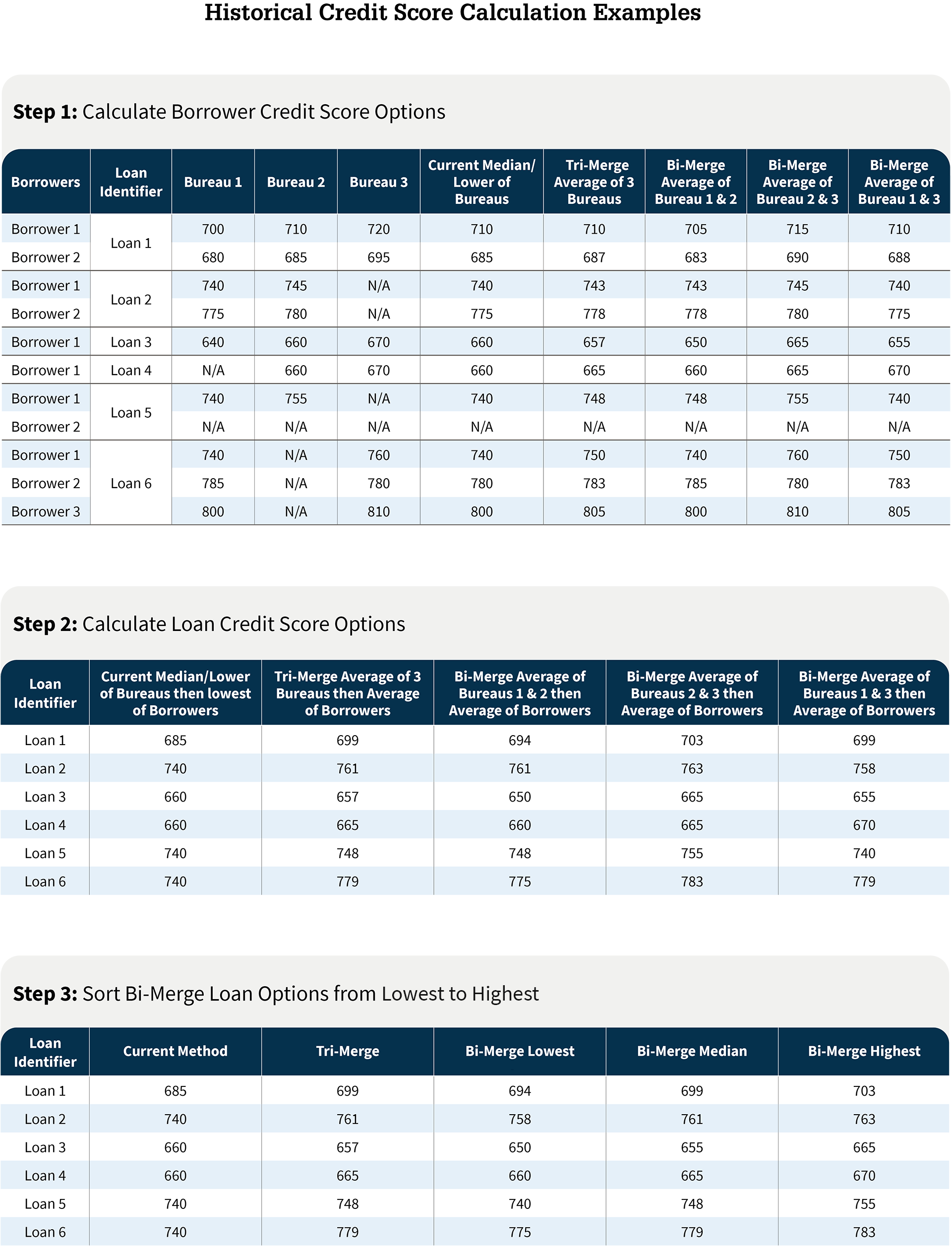

Q12. What loan-level credit score calculation methodology was used to produce the FICO Score 10T and VantageScore 4.0 historical credit scores?

The FICO Score 10T and VantageScore 4.0 historical credit scores were calculated using two methods: Our current Middle/Lower then Lowest methodology and the proposed new Average then Average methodology.

Current Methodology: Uses the tri-merge Middle/Lower then Lowest methodology, where the middle of the three or lower of the two credit bureau scores is selected for each borrower, and then the lowest score of all borrowers on the loan is chosen. The Classic FICO calculation methodology will not be changing, and the data is already available through the existing disclosure datasets.

Proposed New Methodology: In the Average then Average methodology, the available credit scores from each credit bureau for each borrower are averaged. If there is more than one borrower, then a simple average of all the borrowers’ average credit scores is calculated.

Q13. How are the values included in the FICO Score 10T and VantageScore 4.0 datasets for the bi-merge lowest, median, and highest fields calculated?

The bi-merge credit scores reflect data from the credit bureaus: Equifax, Experian and TransUnion. For each borrower on the loan, the average of each pairing of the credit bureaus is collected, i.e., the average of the Equifax and Experian scores, the average of the Equifax and TransUnion scores, and the average of the Experian and TransUnion scores. The loan-level credit score is then determined by averaging each borrowers' average of each pairing of the credit bureaus, i.e., the average of all the borrower’s average of the Equifax and Experian, etc. These scores are then ranked from lowest to highest, with the specific bureau combinations varying depending on the borrower and the loan. See example below.

A note on rounding: In cases where the aggregated (averaged) values fall between two whole numbers, score values are always rounded to the nearest whole number, meaning that a score with a decimal at or above .5 is rounded up, and below .5 is rounded down. Rounding is conducted at each step in the aggregation process (i.e., scores are rounded when aggregated to the borrower level, as well as when borrower-level scores are aggregated to the loan level).

Need help?

For more information, reach out to your Fannie Mae representative or Contact Us for Technology Support.